All Categories

Featured

Table of Contents

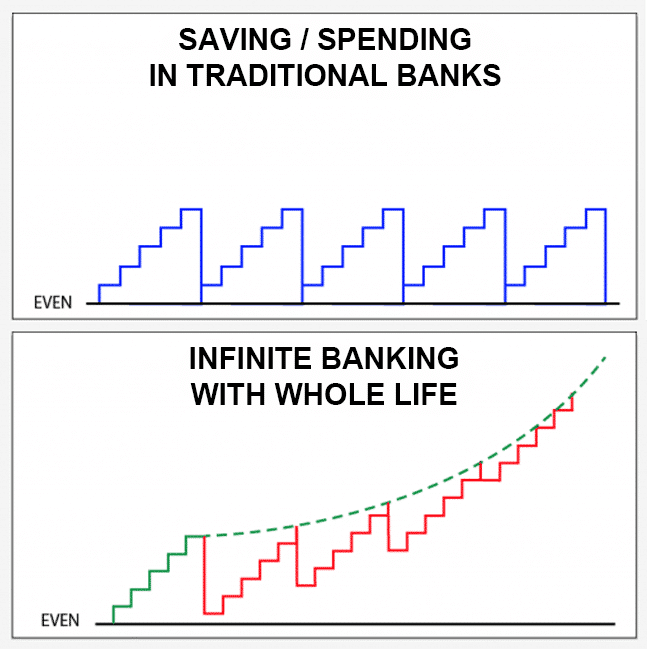

For most individuals, the largest trouble with the unlimited financial concept is that first hit to early liquidity triggered by the prices. Although this disadvantage of boundless banking can be reduced significantly with proper plan layout, the initial years will certainly constantly be the most awful years with any type of Whole Life policy.

That stated, there are specific infinite banking life insurance coverage policies designed mostly for high very early cash money value (HECV) of over 90% in the very first year. Nonetheless, the long-term performance will often substantially delay the best-performing Infinite Banking life insurance policy policies. Having access to that extra 4 figures in the initial few years might come with the expense of 6-figures later on.

You in fact obtain some substantial long-term advantages that help you redeem these early prices and after that some. We locate that this prevented very early liquidity issue with boundless banking is extra psychological than anything else once completely checked out. Actually, if they definitely required every cent of the cash missing out on from their unlimited financial life insurance coverage policy in the very first couple of years.

Tag: infinite banking concept In this episode, I chat regarding finances with Mary Jo Irmen that teaches the Infinite Financial Concept. With the increase of TikTok as an information-sharing system, financial recommendations and approaches have found an unique way of spreading. One such strategy that has actually been making the rounds is the unlimited banking idea, or IBC for short, garnering endorsements from celebs like rap artist Waka Flocka Fire.

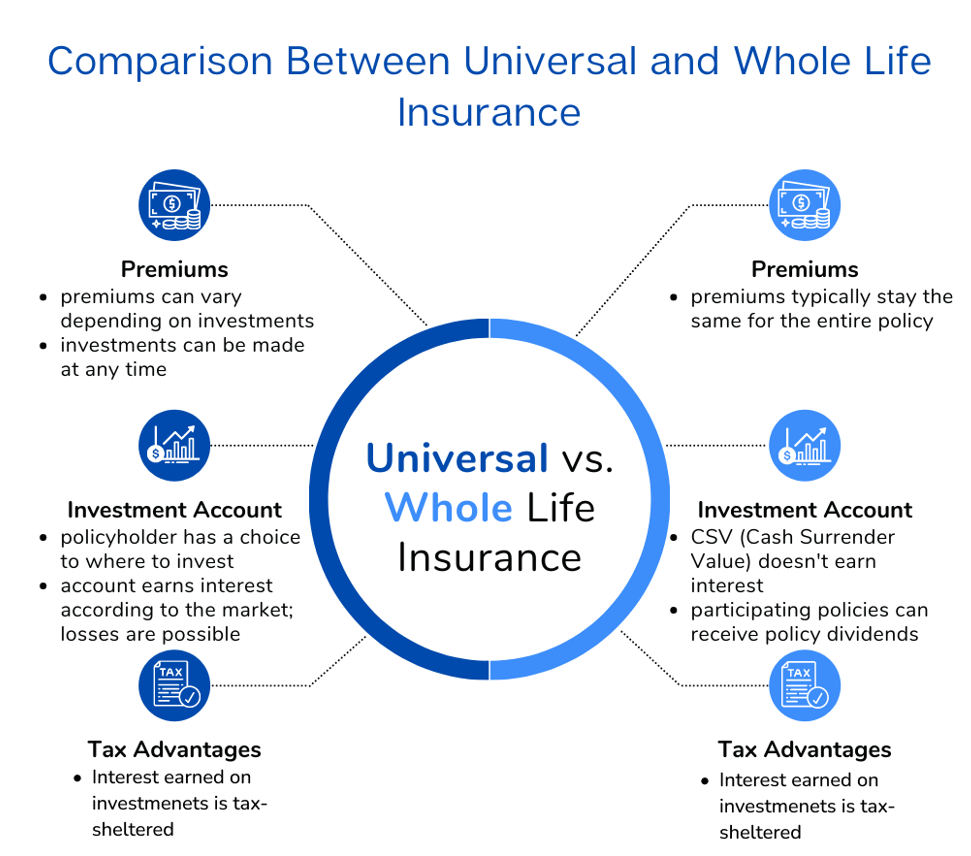

Within these plans, the money value grows based upon a rate established by the insurance provider. Once a significant cash money value builds up, insurance holders can acquire a cash money worth financing. These financings vary from traditional ones, with life insurance coverage acting as collateral, implying one can shed their insurance coverage if borrowing excessively without sufficient money value to sustain the insurance costs.

And while the attraction of these plans appears, there are innate limitations and risks, demanding attentive cash money worth tracking. The strategy's legitimacy isn't black and white. For high-net-worth individuals or entrepreneur, particularly those utilizing methods like company-owned life insurance policy (COLI), the benefits of tax obligation breaks and substance development might be appealing.

Standard Chartered Priority Banking Visa Infinite

The allure of infinite financial does not negate its obstacles: Expense: The fundamental need, an irreversible life insurance coverage policy, is pricier than its term counterparts. Qualification: Not everyone qualifies for entire life insurance policy because of extensive underwriting procedures that can omit those with details health and wellness or lifestyle problems. Complexity and danger: The detailed nature of IBC, paired with its dangers, may prevent several, especially when less complex and much less dangerous alternatives are offered.

Designating around 10% of your month-to-month earnings to the plan is just not practical for a lot of individuals. Part of what you review below is simply a reiteration of what has actually currently been said above.

So prior to you obtain right into a scenario you're not gotten ready for, understand the following initially: Although the concept is generally marketed as such, you're not really taking a car loan from yourself. If that held true, you wouldn't need to settle it. Instead, you're borrowing from the insurer and have to settle it with rate of interest.

Some social media blog posts recommend utilizing cash money value from whole life insurance policy to pay down credit report card financial obligation. When you pay back the loan, a part of that passion goes to the insurance business.

For the initial several years, you'll be paying off the payment. This makes it extremely tough for your plan to build up value during this time. Unless you can pay for to pay a few to several hundred bucks for the next years or more, IBC won't function for you.

Infinite Banking Concept Calculator

If you call for life insurance policy, below are some important pointers to take into consideration: Think about term life insurance coverage. Make certain to shop about for the ideal price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Typeface Name "Montserrat". This Font style Software is licensed under the SIL Open Font License, Variation 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Font Style Call "Montserrat". This Typeface Software application is licensed under the SIL Open Font Style Permit, Variation 1.1.Avoid to main material

How Does Infinite Banking Work

As a certified public accountant concentrating on actual estate investing, I've cleaned shoulders with the "Infinite Financial Concept" (IBC) more times than I can count. I've even spoken with professionals on the subject. The major draw, in addition to the evident life insurance policy benefits, was always the idea of building up cash money worth within a permanent life insurance policy plan and borrowing against it.

Certain, that makes good sense. Truthfully, I constantly assumed that money would certainly be better invested straight on investments instead than funneling it with a life insurance plan Until I found just how IBC could be combined with an Irrevocable Life Insurance Coverage Trust Fund (ILIT) to develop generational wide range. Allow's start with the basics.

Infinite Banking Vs Bank On Yourself

When you obtain versus your policy's cash money value, there's no set repayment timetable, providing you the freedom to manage the financing on your terms. The money value continues to grow based on the policy's warranties and returns. This configuration allows you to gain access to liquidity without interrupting the long-term growth of your plan, offered that the car loan and interest are taken care of intelligently.

As grandchildren are birthed and expand up, the ILIT can acquire life insurance plans on their lives. Family members can take financings from the ILIT, making use of the money worth of the plans to fund investments, begin businesses, or cover major expenses.

A critical facet of managing this Family Bank is the usage of the HEMS requirement, which means "Wellness, Education And Learning, Maintenance, or Assistance." This guideline is usually included in depend on agreements to guide the trustee on how they can distribute funds to recipients. By adhering to the HEMS criterion, the count on guarantees that circulations are made for important requirements and long-lasting assistance, guarding the depend on's assets while still offering member of the family.

Increased Versatility: Unlike rigid small business loan, you regulate the repayment terms when obtaining from your very own policy. This allows you to framework repayments in a manner that straightens with your organization capital. infinite financial systems. Better Cash Money Circulation: By funding service expenses with policy fundings, you can potentially release up money that would certainly otherwise be locked up in typical funding repayments or tools leases

He has the exact same devices, but has also built added money value in his policy and received tax benefits. And also, he currently has $50,000 readily available in his plan to make use of for future opportunities or expenses., it's crucial to view it as more than simply life insurance.

Infinite Banking With Whole Life Insurance

It's about creating a versatile financing system that offers you control and provides numerous benefits. When utilized tactically, it can complement various other financial investments and company methods. If you're fascinated by the potential of the Infinite Banking Idea for your organization, right here are some steps to think about: Educate Yourself: Dive deeper right into the concept through trusted publications, workshops, or examinations with knowledgeable professionals.

{kind=link}

Latest Posts

How Can I Be My Own Bank

Self Banking Concept

Becoming Your Own Banker : The Infinite Banking Concept ...